Further Decline in Inflation in February Will Keep the Bank of Canada On Hold in April

All eyes will be on the Federal Reserve tomorrow when they decide whether to hold rates steady because of the banking crisis or raise the overnight rate by 25 basis points (bps). Before the run on Silicon Valley Bank, markets were betting the Fed would go a full 50 bps tomorrow, as Chairman Powell intimated to the House and Senate.

Since then, three bank failures in the US as well as the UBS absorption of troubled Credit Suisse, have caused interest rates to plummet, bank stocks to plunge, and credit conditions to tighten. Many worry that rate increases will exacerbate a volatile situation, but others believe the Fed should continue the inflation fight and use Fed lending to provide liquidity to financial institutions.

Relative calm has been restored thanks to the provision of huge sums of emergency cash by lenders of last resort–the central banks–and some of the US industry’s strongest players.

While Canadian bank stocks have also been hit, the banks themselves are in far better shape than the weaker institutions in the US. Our banks are more tightly regulated, have much more plentiful Tier 1 capital, and their outstanding loans and depositors are far more diversified.

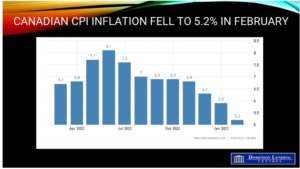

This morning, Statistics Canada released the February Consumer Price Index (CPI). Headline inflation fell more than expected to 5.2% from 5.9% in January. This was the largest deceleration in the headline CPI since the beginning of the pandemic in April 2020.

The year-over-year deceleration in February 2023 was due to a base-year effect for the second consecutive month, which is attributable to a steep monthly increase in prices in February 2022 (+1.0%).

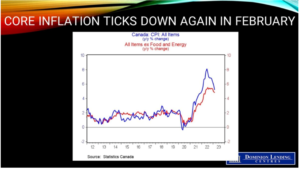

Excluding food and energy, prices were up 4.8% year over year in February 2023, following a 4.9% gain in January, while the all-items excluding mortgage interest cost rose 4.7% after increasing 5.4% in January.

On a monthly basis, the CPI was up 0.4% in February, following a 0.5% gain in January. Compared with January, Canadians paid more in mortgage interest costs in February, partially offset by a decline in energy prices. On a seasonally adjusted monthly basis, the CPI rose 0.1%.

While inflation has slowed in recent months, having increased by 1.2% compared with 6 months ago, prices remain elevated. Compared with 18 months ago, for example, inflation has increased by 8.3%.

Food prices continued to rise sharply–up 10.6% y/y, marking the seventh consecutive month of double-digit increases. Supply constraints amid unfavourable weather in growing regions and higher input costs such as animal feed, energy and packaging materials continue to put upward pressure on grocery prices.

Price growth for some food items such as cereal products (+14.8%), sugar and confectionary (+6.0%) and fish, seafood and other marine products (+7.4%) accelerated on a year-over-year basis in February.

Prices for fruit juices were up 15.7% year over year in February, following a 5.2% gain in January. The increase was led by higher prices for orange juice, as the supply of oranges has been impacted by citrus greening disease and climate-related events, such as Hurricane Ian.

In February, energy prices fell 0.6% year over year, following a 5.4% increase in January. Gasoline prices (-4.7%) led the drop, the first yearly decline since January 2021. The year-over-year decrease in gasoline prices is partly the result of a base-year effect, as prices began to rise rapidly in the early months of 2022 during the Russian invasion of Ukraine.

Shelter costs rose at a slower pace year-over-year for the third consecutive month, rising 6.1% in February after an increase of 6.6% in January. The homeowners’ replacement cost index, related to the price of new homes, slowed on a year-over-year basis in February (+3.3%) compared with January (+4.3%). Other owned accommodation expenses (+0.2%), which include commissions on the sale of real estate, also decelerated in February. These movements reflect a general cooling of the housing market.

Conversely, the mortgage interest cost index increased at a faster rate year over year in February (+23.9%) compared with January (+21.2%), the fastest pace since July 1982. The increase occurred amid a higher interest rate environment.

Bottom Line

The Bank of Canada is no doubt delighted that inflation continues to cool. Canada’s inflation rate is low compared to the US at 6.0% last month, the UK at 10.1%, the Euro Area at 8.5%, and Australia at 7.2%.

The Bank was already in pause mode and will likely stay there when they meet again in April

(Dr. Sherry Cooper. Chief Economist, Dominion Lending Centres)